“There’s an old saying in Tennessee — I know it’s in Texas, probably in Tennessee — that says, fool me once, shame on — shame on you. Fool me — you can’t get fooled again.”

We are short Applied Optoelectronics (“AAOI”, “Applied”, “the Company”), a manufacturer of optical transceivers and networking components used in data centers and cable television equipment. AAOI claims its next-generation 800G transceivers have been undergoing qualifications representing “more than $500 million or even $600 million“ in revenues, but our research – including 20+ interviews with former AAOI employees, competitors, hyperscalers, and industry experts, as well as our visits to AAOI’s facilities – suggests that AAOI has wildly misrepresented its 800G prospects, cannot scale 800G production as claimed, and has already squandered its chances with potential customers.

AAOI first claimed in Q3 2023 that, “we shipped samples of our 800G transceivers to 2 different customers… by the end of the year, we expect to ship samples of 800G products to 2 additional datacenter customers.” However, both a former AAOI employee and a major hyperscaler suggested to us that AAOI never shipped 800G samples in Q3 2023, and these weren’t ready until 9-12 months later. According to a former Meta employee:

“The RFQ was opened end of 2023, then closed first quarter 2024… For 800G we got the first samples in, and some testing was going on for 800G. Today, 800 is being deployed… We did not see any supplies from Applied. Applied said they’d get us 800G in 3 quarters. But the RFQ was closed by the time Applied could get us samples.” – Former Meta employee

“From the time I was there until the time I left [summer 2024], 800G was actively worked on, but that product was not released by the time I left… September 2024 release, that’s what they had planned.” – Former AAOI employee

According to multiple experts we spoke with, qualification is a 3- to 9-month process, suggesting that if AAOI had been shipping samples as claimed in Q3 2023, we already should have seen the Company report multiple qualifications. Tellingly, AAOI remains without a single disclosed 800G customer today, and has already pushed back 800G revenue expectations by 3 quarters.

In Q3 2024, AAOI claimed to have “re-engaged” another hyperscaler customer later understood to be Amazon.1 AAOI claimed, “We are in a position to ramp production to meet their needs, and have already received some small initial orders with additional orders expected in Q4 and into 2025.” Yet according to multiple sources we spoke with, after AAOI shipped an initial batch of products in September 2024, Amazon became “pissed off” with Applied, after finding that the Company over-promised on its production abilities:

“Amazon was pissed off. They [AAOI] said that they could do it, and then they didn’t. That was this past September… you promise you’re going to ship this brand new technology, and it’s not that easy to ramp up… They [AAOI] simply don’t have capacity to do it…” – Source #1

“[AAOI] sent out samples to Amazon on the DR8 [800G module]… That was September or October last year. Applied is not a qualified vendor at Amazon right now for 400G or 800G. I can tell you that. They may be trying to figure it out, but I know that they tried and haven’t.”2 – Source #2

We also find AAOI misrepresents its existing relationship with Microsoft. The Company claims Microsoft could generate over $300 million in revenues in “400G and beyond” yet the agreements appear to have no minimum purchase obligations, and revenue has been limited to low-end products and cables. Instead, Microsoft has already been deploying 800G transceivers from competitors. According to one Microsoft employee:

“A few years ago 400G was our standard, now 800G is our standard… The stuff we’re working on with them [AAOI], there’s been limited shipping. It’s not full production value…”

“We’ve been deploying all the 800G stuff with InnoLight and Lumentum and Coherent.”

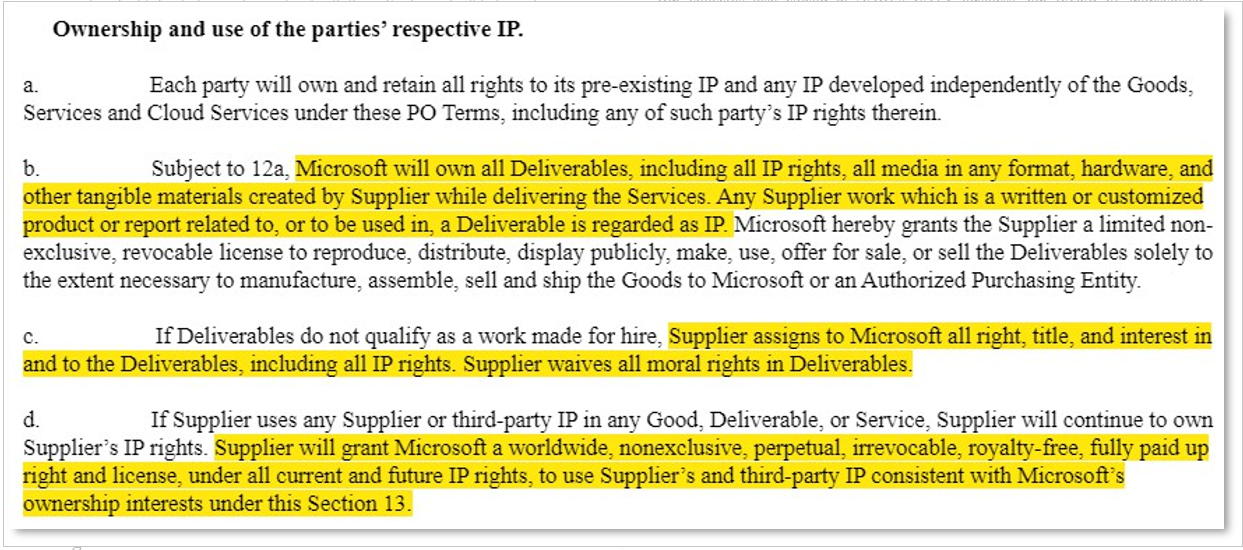

AAOI further suggests that Microsoft provides validation and leverage to win new customers, but we believe it’s the exact opposite – AAOI is Microsoft’s pawn – a bargaining chip and a backup plan when it comes to 800G. Microsoft retains the IP and exclusivity over the work product, restricting AAOI’s ability to use it elsewhere.3 As one Microsoft employee told us, “those things are our property.”

Our research also uncovered problems across AAOI’s manufacturing facilities in China, Taiwan, and the U.S. We believe that even if AAOI had any 800G customer qualifications, the Company remains incapable of ramping 800G production in Q1 2025 as management has promised, even after repeatedly pushing back timelines.

- In 2022, AAOI attempted to sell its Chinese transceiver manufacturing assets, but the buyers backed out of the deal. Chinese media reports as of January 2024 suggest the buyers ultimately found the assets “not very great.” We spoke with an executive at a competitor who was pitched the opportunity to buy the facility, who told us, “we kicked the tires, had a good laugh, and said not a chance, there’s nothing .. Those lines cannot produce 800G in any meaningful way.”

- Just three weeks ago, we visited the Company’s expansion site in Taiwan. Our investigator found an empty facility that we believe is clearly incapable of any near-term production.

- CEO Lin claims that U.S. production is possible with a “similar or a bit higher cost than in Taiwan and China” which is “very attractive to the customer.” Yet multiple experts told us that meaningful U.S. production is a non-starter, as “it’s too expensive” and “the labor rate is way too high… 3x more…” while customers have no incentive to pay higher prices for a commodity product made by a vendor with a highly checkered past.4

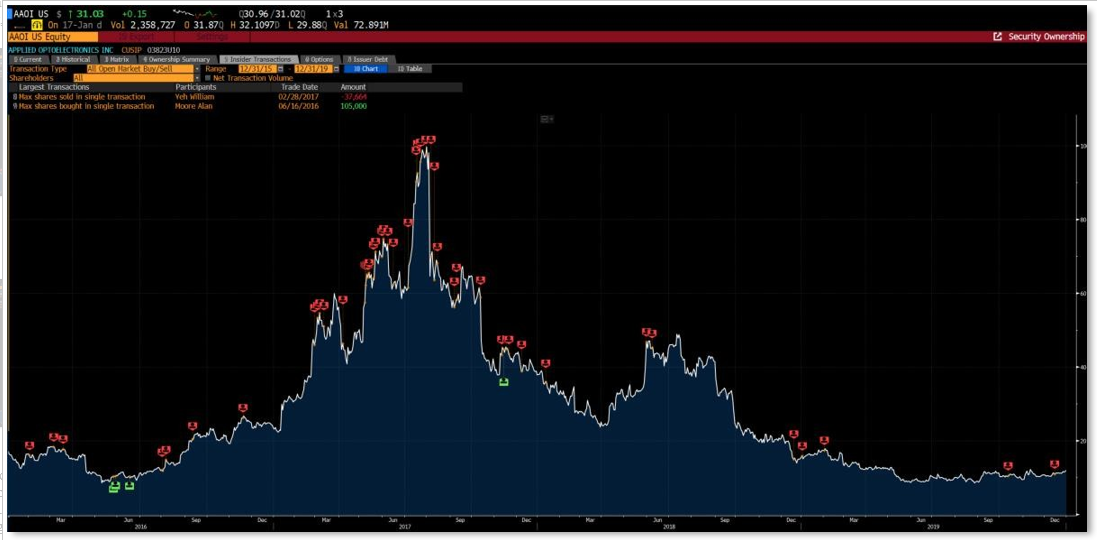

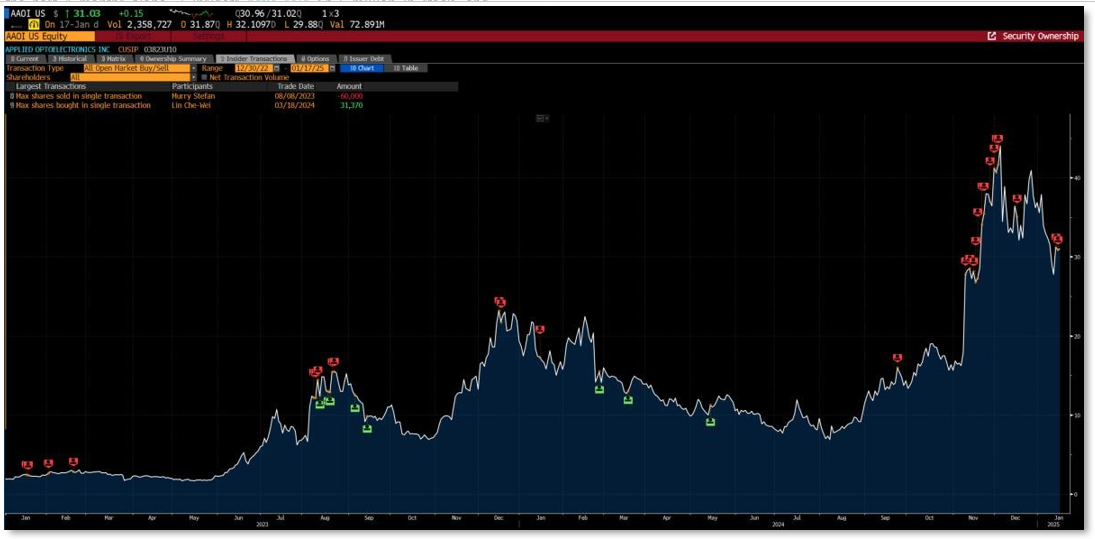

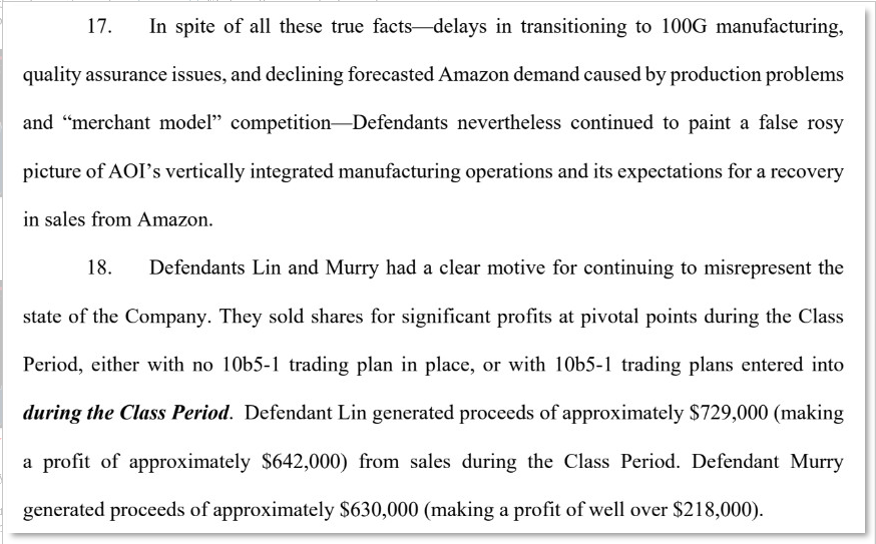

We’ve seen this story play out before. Between 2016 and 2017, AAOI claimed massive demand for 100G modules would transform its business. Shares rose over 800%, and insiders unloaded millions in stock. However, AAOI allegedly hid product quality issues, manufacturing setbacks, and declining customer demand forecasts. As these problems were revealed, shares fell over 90% from highs, and the Company settled multiple securities fraud lawsuits. Nevertheless, CEO Lin and CFO Murry remain at AAOI today, and insiders are once again selling stock – seven insiders have sold stock in the last four months alone. Numerous industry participants expressed that this history has alienated potential customers, who have effectively blacklisted AAOI as a supplier.

“The industry hasn’t forgotten. They all remember what happened. So AAOI’s been tarnished, and that’s why they still languish… At Nvidia, it’s not just no, but hell no.” – AAOI Competitor #1

“The general market perception is that Coherent and Lumentum fail less.” – Former at Top 5 Hyperscaler

“Nvidia wouldn’t work with them.” – AAOI Competitor #2

“It’s hard for me to believe from the outside looking how they’re going to execute this time… if it’s the same people, same leadership, same management, they’re doing a repeat.” – AAOI Competitor #3

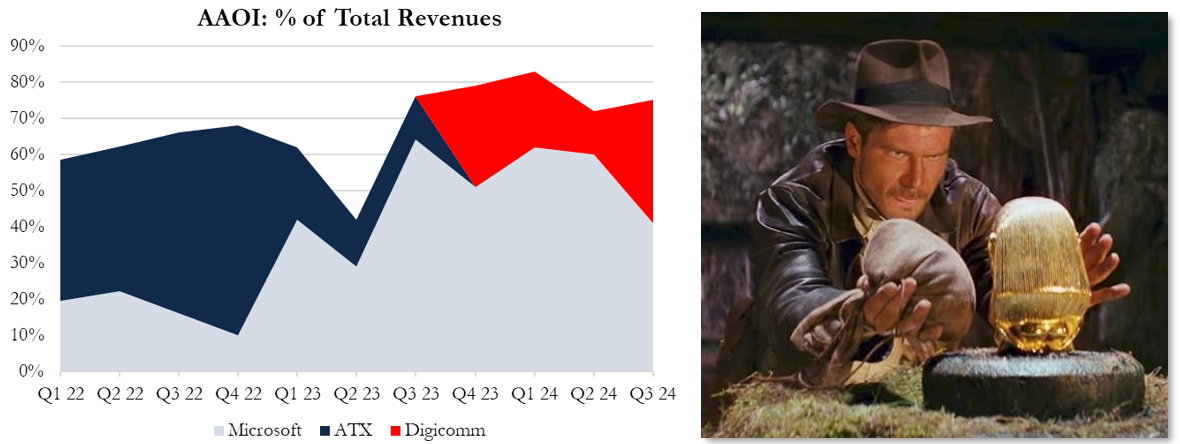

Our research also uncovered significant issues in AAOI’s CATV business, including an undisclosed lawsuit stemming from the loss of AAOI’s largest customer, tariff evasion, and channel stuffing.

- In September 2023, AAOI sued its then-largest customer, ATX Networks, alleging breach of contract (i.e., unpaid bills). ATX’s response alleged that the unpaid balances resulted from overbilling, the difference owing largely to differences in “anticipated tariff liabilities.” Sources suggested to us that ATX took issue with AAOI’s practice of routing Chinese products through Taiwan to avoid tariffs. Our detailed review of import/export records corroborates these concerns. ATX represented 47% of AAOI’s 2022 revenues, but has fallen below 10% today, while sources tell us ATX and AAOI are now competitors, not partners. Despite the obvious materiality, AAOI has never disclosed the litigation or loss of ATX, underscoring our concerns of management transparency.

- In November 2023 – just two months after losing ATX – AAOI signed a distribution agreement with Digicomm. We believe this deal allowed AAOI to push product to Digicomm in order to support guidance, while papering over the undisclosed litigation and loss of ATX. Experts expressed skepticism that AAOI’s sales into Digicomm were based on underlying demand, stating, “If you want to call it channel stuffing, we used that exact same terminology…” AAOI’s financials reveal that while AAOI recognized $16.9 million in revenues from Digicomm in the fourth quarter, the entire balance remained unpaid at year-end.

Intro to Applied Optoelectronics: a Subscale Commodity Transceiver Manufacturer

Applied Optoelectronics was founded in 1997 and manufactures optical transceivers and other fiber optic access networking components. Transceivers are small packages of lasers and circuits that convert light to electrical signals and vice versa, utilized primarily in data centers, telecom equipment, and cable television. Components are classified by bandwidth i.e., 10G, 40G, 100G, 400G, 800G, 1.6T, and beyond. Lower bandwidths are capable of broadband access and telecom applications, while demand for 400G, 800G, and 1.6T transceivers has been driven by data center buildouts for artificial intelligence (“AI”) applications

Transceivers are standardized, commoditized products offered by numerous suppliers. Given rapid upgrade cycles, (i.e., 40G to 100G; 100G to 800G) and accompanying deflation, AAOI’s business is brutally competitive.

“We don’t see a lot of distinction… generally speaking, they all stay pretty competitive with each other. It becomes a scale and capability game…” – Hyperscaler purchaser #1

“They are in a commodity market where they have to fight on pricing.” – Hyperscaler purchaser #2

“Transceivers are pretty ubiquitous.” – AAOI competitor #1

“The problem is the market is very competitive… There are probably 20 companies in the world today who can support transceiver business.” – AAOI competitor #2

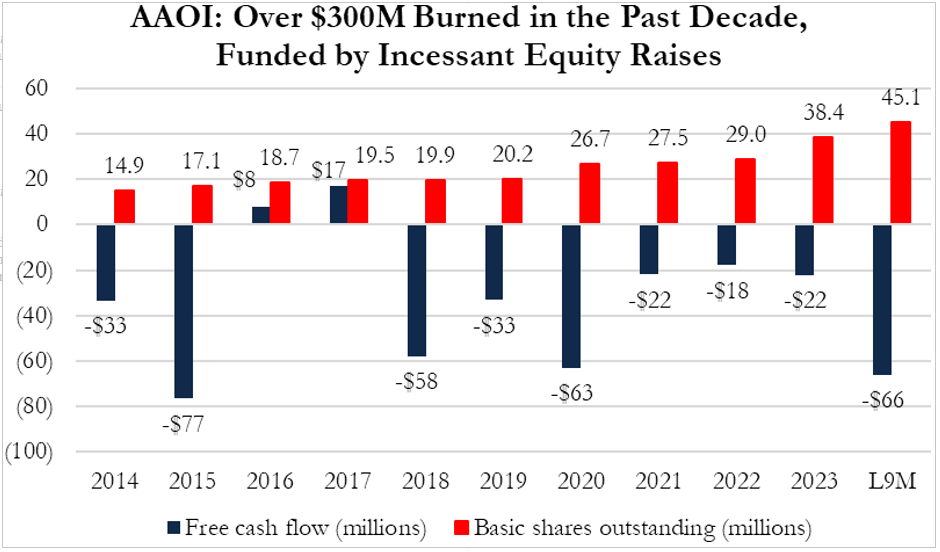

AAOI is subscale and has been dominated by its competitors. Over the past 10 years, AAOI has burned $301 million, funded by constant equity issuances. Share count has ballooned from 14.9 to 45.1 million today.

We Believe AAOI Has Misrepresented 800G Development and Qualifications

In Q3 2023, AAOI claimed that the Company shipped 800G product samples to two potential data center customers, underpinning CEO Lin’s calls to “more than $500 million or even $600 million” in 800G revenues.5 According to CFO Murry:

“During the quarter, we shipped samples of our 800G datacenter products to 2 different customers. By the end of the year, we expect to ship samples of 800G products to 2 additional datacenter customers. This would bring our total to 4 different datacenter customers who would be evaluating our 800G products by year-end.”

However, according to both former employees and hyperscalers that we spoke with, AAOI was never able to ship 800G samples when claimed, and the products weren’t ready until 9 to 12 months later.

Both Former AAOI Employee and Hyperscalers Contradict AAOI’s Claims of Q3 2023 Shipments

We interviewed a former employee at Meta who was responsible for sourcing the hyperscaler’s 800G transceivers. They told us that – in contrast to AAOI’s Q3 2023 claims to have shipped product samples – AAOI was never even considered for Meta’s RFQ for 800G, as AAOI was unable to produce sample products by the time the RFQ closed in Q1 2024:

“The RFQ was opened end of 2023, then closed first quarter 2024… For 800G we got the first samples in, and some testing was going on for 800G. Today [January 2025] 800 is being deployed… We did not see any supplies from Applied. Applied said they’d get us 800G in 3 quarters [Q3 2024]. But the RFQ was closed by the time Applied could get us samples.”

A former high-level employee at AAOI independently corroborated both aspects of this account, stating that AAOI did not have 800G ready in 2023, but instead had planned to for a September 2024 release:

“From the time I was there until the time I left [summer 2024], 800G was actively worked on, but that product was not released by the time I left… September 2024 release, that’s what they had planned.”

Notably, AAOI’s 2023 Form 10-K never disclosed 800G development as a material driver of R&D expenses, even as the disclosures called out numerous other business lines, and as CEO Lin stated on the Q3 call months earlier, “that’s why we are putting our resource[s] into 800G and the 1.6T business…” According to the 10-K:

“Research and development expense decreased $0.27 million, or 0.7% from 2022 to 2023. Research and development costs consist of R&D work orders, R&D material usage and other project related costs related to 100 Gbps, 200/400 Gbps data center products, DOCSIS 4.0 capable CATV products, including

1.8 GHz-capable amplifier products, and other new product development…”

Experts we spoke with suggested that even if AAOI had shipped samples to Meta, the hyperscaler would be unlikely to buy from AAOI given incumbent relationships and AAOI’s checkered history. According to one, “Meta is a customer of a customer of Lumentum and Coherent. They wouldn’t risk much going with other suppliers.” Another expert we spoke with had an even more critical view, emphasizing that because of AAOI’s widely recognized past failings in servicing Meta (then Facebook) during the 40G to 100G upgrade cycle, “Meta will never touch them again.”6

AAOI Claims Ramping Production for Amazon. Sources Say AMZN Was “Pissed Off ” and Walked

On AAOI’s Q3 2024 conference call in November, CFO Murry claimed that AAOI has had “meaningful conversations” with another hyperscaler and expects ramping orders from that customer in Q4 2024 and 2025.

“…we have had meaningful conversations with an additional hyperscale customer who has begun to reengage with us in preparation for future data center upgrades. We are in a position to ramp production to meet their needs and have already received some small initial orders with additional orders expected in Q4 and into 2025.”

According to sell-side notes and our interviews with industry experts, this hyperscaler is now understood to be Amazon. However, our research suggests that while Amazon did order a batch of transceivers from AAOI in September 2024, AAOI over-promised on both the scale of its capacity and production timelines, and Amazon ditched AAOI in favor of competitors. According to our interview with one familiar source:

“Amazon was pissed off. They [AAOI] said that they could do it, and then they didn’t. That was this past September… they didn’t have the capacity… you promise you’re going to ship this brand new technology, and it’s not that easy to ramp up the brand new technology… They [AAOI] simply don’t have capacity to do it… Overpromising on the quantity and the timelines…

A second source corroborated this timeline of events, stating in our January 2025 interview that:

“[AAOI] sent out samples to Amazon on the DR8 [800G module]… That was September or October last year. Applied is not a qualified vendor at Amazon right now for 400G or 800G. I can tell you that. They may be trying to figure it out, but I know that they tried and haven’t.”

We believe Amazon turned down AAOI in favor of Jabil (JBL), which has its own optical transceiver business, bolstered by the October 2023 acquisition of Intel’s silicon photonics transceiver unit. In late September 2024, Amazon formed a strategic alliance with Jabil, and further in January 2025, Amazon announced an investment in Jabil. Signing the warrant agreement on Jabil’s behalf was Matthew Crowley, EVP of Jabil’s “Intelligent Infrastructure” segment, which includes Jabil’s offerings for what it calls “next-wave cloud and AI data centers.” Previously, Crowley was employed by Amazon’s AWS. One source opined to us that “Jabil is going to be manufacturing all that [transceivers]” and when we asked about AAOI’s chances of securing any future 800G business with Amazon, said, “I wouldn’t count on it.”

AAOI Claims Ongoing Qualifications, But Continually Pushes Back 800G Revenue Expectations

Since AAOI first claimed to ship 800G samples in Q3 2023, the Company has continually pushed back 800G revenue expectations. According to multiple AAOI competitors and hyperscalers we spoke with, full qualification – from RFP/RFQ issuance to final acceptance – is typically completed in 3 to 12 months.7 As such, we would have expected AAOI to have disclosed multiple qualifications by now, but the Company has disclosed none. This suggests to us either that the Company didn’t actually ship products in Q3 2023 as claimed, or the Company is harboring production problems, or both.

AAOI’s Production Footprint Lacks the Ability to Meet Expectations

We believe that – even if AAOI had any qualified 800G customers – the Company’s manufacturing footprint is wholly incapable of delivering on the Company’s promises of material 800G revenues in Q1 2025 and “hundreds of millions” in 800G revenues over the next few years.

In 2022, AAOI Tried and Failed to Sell Chinese Manufacturing Assets. Buyers Called the Assets

“Not Very Attractive.” Another Potential Buyer We Spoke with Said “We Laughed… Nothing Here”

AAOI holds production facilities in Ningbo, China (458,849 square feet), Taipei, Taiwan (268,797 square feet), and Sugar Land, Texas (139,450 square feet).8 We believe that the Company’s China-based facilities are not only rife with geopolitical risk, but incapable of producing 800G at scale without massive capex.

In September 2022, AAOI announced an agreement to sell its Chinese facilities to Yuhan Optoelectronic Technology Co. (“Yuhan”), supported by an investment into Yuhan by Henan Shijia Photonics Technology Co., Ltd. (“Shijia”). However, in September 2023, AAOI terminated the deal citing “Yuhan’s failure to meet agreed upon deadlines…” while reiterating that “we are exploring additional options with new potential buyers.”9 January 2024 media reports suggested that original Chinese buyers found the assets unattractive:

“In terms of the production capacity of the optical module industry and the technological leadership of its own AOI optical module business, the attractiveness of AOI-related assets is not so great for the leading domestic manufacturers.”

We attempted to tour AAOI’s China facilities, but were denied entry. However, we spoke with another potential buyer who had toured the assets, but called them “obsolete” and incapable of meaningful 800G production:

“[It is a] rather obsolete factory in China. We kicked the tires but we had a good laugh and said not a chance, there’s nothing here…”

“The manufacturing lines themselves that are used for 100G transceivers. Those lines cannot produce 800G in any meaningful way. They can produce 400G, that’s fine, but there’s a sea change in manufacturing technology required… It’s much better to do it from the ground up, if you have the money.”

AAOI’s Expansion in Taiwan Appears Wholly Incapable of Scaling for Q1 2025 Production

AAOI claims that the Company can “execute on the revenue growth trajectory that we outlined” by expanding production in the U.S. and Taiwan, and that 800G is set to while further maintaining that 800G revenues will come in Q4 2024 and “should start to ramp in Q1” 2025. However, we’ve found neither the Company’s U.S. nor Taiwanese facilities capable of profitable 800G production, putting these calls to “ramping” production in doubt.10

In Taiwan, AAOI only signed an agreement to build an expansion on December 26, 2024. We visited the site three weeks ago. As shown below, our investigator spoke with the site foreman, who directed us to the “additional production facility for the head office.”

While some materials were present on site, the facility was a far cry from being ready for commercial production. It’s unclear to us how AAOI claimed to ramp production given the facility won’t even be built until Q2.

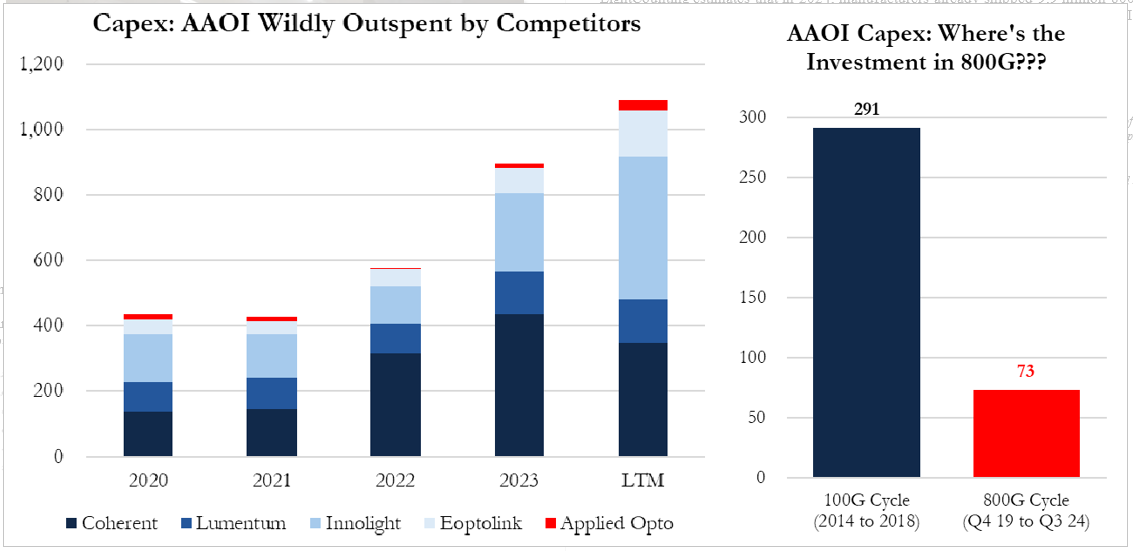

By contrast, consider that peers such as Coherent (COHR) have been wildly outspending AAOI well in advance of demand.11 Further, AAOI has not even met its own past spending standards: in the prior 100G cycle, AAOI spent $291 million in capex, but in anticipation of this cycle, AAOI has spent just $73 million in capex.12

LightCounting estimates that in 2024, manufacturers already shipped 9.9 million 800G transceivers worth $5.1 billion – competitors are now reaping the rewards, and AAOI is still out to lunch.

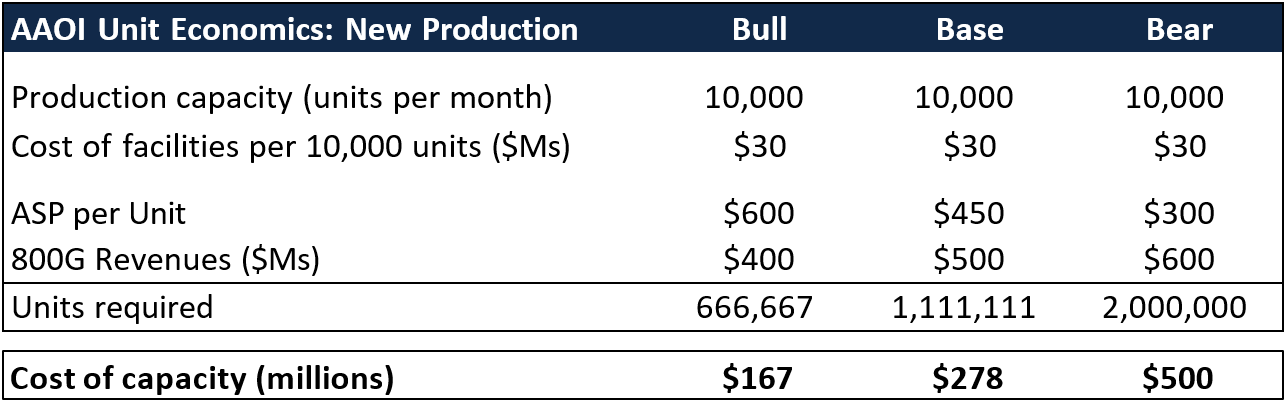

AAOI Would Need to Spend Hundreds of Millions Expanding Capacity to Meet 800G Claims

We estimate AAOI needs to spend $167 to $500 million in capex in order to have any chance of seeing the “$500 or even $600 million” in 800G opportunities touted by management. To our knowledge, AAOI has not publicly disclosed its intended capex from 2024 to 2026, but one sell-side note we reviewed suggested that the Company could support 800G sales of “hundreds of millions of dollars” for just $50 million in spending (the analyst doesn’t disclose any assumptions).13 We think the true costs would be several multiples higher.

One optical veteran told us it would cost AAOI “$100 million in equipment and facilities” in order to support a doubling from ~$200 million to ~$400 million in revenues, implying that the Company would first need to spend

$300 million to see an incremental $600 million in revenues as CEO Lin has touted. Another industry veteran told us that the industry-wide rule of thumb contemplates a cost of $40 million to build capacity for 10,000 units per month, with per-unit costs decreasing with scale. With these comments in mind – alongside what we believe are conservative ASP assumptions in a market characterized by rapid price deflation – our estimates of AAOI’s capital spending needs are shown below.14

Finally, with respect to the U.S., CEO Lin claimed on the Company’s Q1 2024 call in May 2024 that “We can do 800G manufacturer in Houston with, I would say, similar or a bit higher cost than in Taiwan and China. I think that’s very attractive to the customer…” We view building out U.S. production as prohibitively expensive, especially in light of AAOI’s already horrific cash burn. According to one competing transceiver manufacturer, “You couldn’t do it in Texas or even in Taiwan… it’s too expensive.” According to another manufacturer we spoke with, “The labor rate is way too high. You’re paying 3x more…” AAOI would thus be faced with the decision to either attempt to charge higher prices or generate even worse operating losses. Yet hyperscalers have no desire to pay higher prices for a commodity product from a manufacturer with a highly checkered past. According to one competitor, “You’ll need to have a price premium… they’ll just go for the cheaper option. There’s no reason.”

We’ve Seen This Movie Before – AAOI Shares Declined Over 90%

In our view, the current situation – characterized by AAOI’s misleading claims of its product qualifications, customer relationships, and production capabilities – appears remarkably similar to the prior 40G to 100G upgrade cycle. CFO Murry claims that the current cycle “could be greater and longer duration” than the 40G to 100G upgrade cycle. Yet for AAOI, the 100G cycle was an unmitigated disaster, and shares declined over 90%. CEO Lin and CFO Murry remain in place today, and despite AAOI’s constant cheerleading, insiders are selling stock. In the past 4 months alone, 7 insiders have sold $6.1 million in stock, and counting, through both 10b5-1 plans and open market sales.

January 2016 to December 2019: AAOI Shares Fall Over 90% on 100G Cycle

January 2023 to the Present: To Be Determined…

Throughout 2016 and early 2017, AAOI touted its ability to supply 100G transceivers to data center customers, and see growth from “all 3 of our customers”, including Amazon. However, the Company allegedly failed to disclose manufacturing issues and declining forecasts. As summarized by subsequent litigation:

Case No. 4:17-cv-2399, Southern District of Texas Houston Division

In November 2017 – just months after losing Amazon – AAOI signed an agreement with Facebook, claiming that that Facebook would purchase products in 2018 and “provided a forecast to make additional purchases in years 2019 through 2020.” On AAOI’s subsequent February 2018 conference call, CFO Murry claimed, “it represents a 3-year timeframe with a minimum commitment for the first year that represents, at a minimum $125 million for one product family. Not all the products, but just one product family.”

However, in September 2018 – on the heels of an independent report suggesting that AAOI’s Facebook business was at risk, the very next day, the Company issued a press release disclosing that indeed, there was “an issue with a small percentage of 25G lasers within a specific customer environment.” AAOI lowered Q3 2018 revenue guidance from $85.5 million to just $56.5 million at the midpoint. By year-end 2018, shares had

fallen over 80%, and would go on to decline over 90% from highs.

Multiple experts we spoke with emphasized that AAOI’s reputation continues to hinder attempts to win new business, including that Nvidia considers working with AAOI a non-starter due to this history. One even added their view that history is set to repeat:

“In the last 6 or 7 years, the industry hasn’t forgotten. They all remember what happened. So AAOI’s been tarnished, and that’s why they still languish at that revenue level today.”

“At Nvidia, it’s not just no, but hell no.” – AAOI Competitor #2

“I’d doubt they’ll be an Nvidia supplier. Nvidia wouldn’t work with them.” – AAOI Competitor #3

“The general market perception is that Coherent and Lumentum fail less.” – Former at Top 5 Hyperscaler

“But again, the management team is by and large, the same management team… It’s hard for me to believe there’s a cultural shift happening within the organization. It’s hard for me to believe from the outside looking how they’re going to execute this time because this goes up a lot of time. But again, if it’s the same people, same leadership, same management, they’re doing a repeat.” – AAOI Competitor #1

AAOI Misrepresents Microsoft Relationship. MSFT is Using Other 800G Providers

In December 2022, AAOI announced an agreement to provide “Foundry” services to Microsoft. In June 2023, the Company announced a second agreement to provide “Design and Assembly” services to Microsoft. In numerous public appearances since those agreements were signed, we believe AAOI has made blatant misrepresentations of that relationship, as we summarize in the table below.

| AAOI Claim / Investors’ View | Culper View |

|---|---|

| Microsoft deal implies minimum revenues of $300 million over the next several years. | Culper View Microsoft does not have minimum purchase obligations with AAOI. |

| Microsoft deal is a validation of the Company’s offerings in “400G and beyond.” | AAOI’s Microsoft revenues have been generated almost entirely by 100G. |

| Microsoft will rely on AAOI as a primary supplier for its 800G buildouts. | Microsoft is already building 800G with other suppliers, now moving to 1.6T. |

| AAOI can leverage its work with Microsoft to win customers like Google, Meta, and Nvidia. | Microsoft retains IP and exclusivity; AAOI can’t use the same designs elsewhere. |

AAOI continually claims that Microsoft is set to contribute over $300 million in revenues. Per CEO Lin on the Q2 2023 conference call in August 2023:

“…if you kind of look at some of the forecasts that we’ve received from them and the contractual, the minimum contractual levels of manufacturing that they’ve asked us to prepare. That would imply revenue of $300 million plus over the next few years just in those products not counting existing other types of business that they might have.”

In each of the Company’s subsequent quarterly calls, management continues to tout the relationship’s potential in

“400G and beyond.” For example, on the most recent call, CFO Murry stated:

“While not guaranteed, we continue to believe that the revenue opportunity for our 400G and 800G products could be greater and longer duration than the revenue contribution we saw from this customer during the peak of the 40G product cycle, which suggests that revenue from these products may exceed

$300 million over the several years of these buildouts.”

Yet Microsoft has already been building out its data centers with 800G modules from competing suppliers.

According to one Microsoft employee:

“A few years ago 400G was our standard, now 800G is our standard… The stuff we’re working on with them [AAOI], there’s been limited shipping. It’s not full production value.”

“We’ve been deploying all the 800G stuff with InnoLight and Lumentum and Coherent.”

While AAOI suggests a cozy relationship with Microsoft, it looks more to us like Microsoft has used AAOI as an insurance policy and a bargaining chip. According to one industry expert we spoke with:

“Usually, [an] agreement like this, Microsoft obviously has incumbent suppliers… By introducing AOI, they have the leverage and say, okay, if Lumentum, if Coherent, if we don’t perform, I have my guy, I have my InnoLight. Look, I signed a contract with them. So if you don’t behave if you look in the best price supportability and services, I can turn around give AOI business…”

AAOI has also touted the Microsoft agreements as validation of its offerings, supporting its attempts to win new datacenter business.15 Per CFO Murry on the Q4 2023 conference call:

“…the value proposition that we offer to Microsoft is just as strong with other data center operators, and we are working with several of them to evaluate our technology and qualify our products. This includes our 800G products.”

However – notwithstanding the fact that AAOI has yet to disclose a single 800G customer – AAOI’s agreements with Microsoft contain exclusivity clauses in which Microsoft retains ownership of “all IP rights”, restricting AAOI’s ability to use this work with other hyperscalers.

As confirmed by the Microsoft employee we spoke with:

“Those [modules] things we design with them [AAOI], those things are our property. There’s a period of time that they can’t use them with AWS or Google. Those are all proprietary designs to those AI clusters… They can leverage those design concepts, but they can’t take our designs and leverage those designs with Amazon or Google…”

Undisclosed Litigation Unveils New Tariff Evasion and Channel Stuffing Concerns

Our concerns also extend to AAOI’s CATV business: our review of undisclosed September 2023 litigation between AAOI and its former largest customer, ATX Networks, reveals tariff evasion concerns, while AAOI’s subsequent agreement with Digicomm reeks of channel stuffing which allowed the Company to paper over the litigation and loss of ATX.

September 2023: AAOI Loses its Largest Customer, ATX Networks, on Alleged Tariff Games

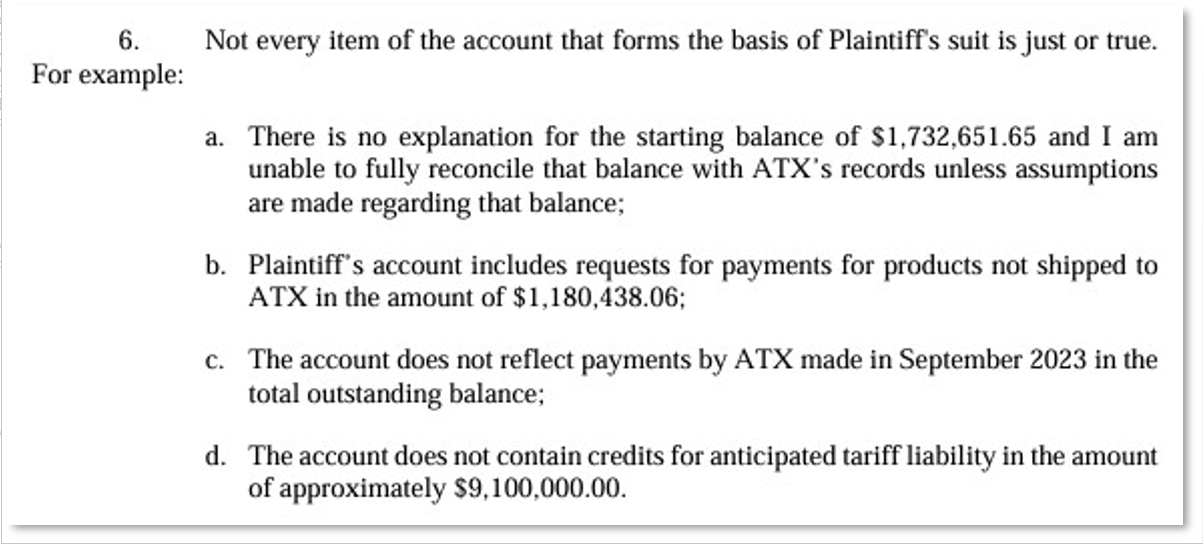

In September 2023, AAOI filed a lawsuit against ATX Networks (“ATX”), which by 2022 had grown to contribute $105 million, or 47% of Company-wide revenues for the year. AAOI has never disclosed this lawsuit nor the subsequent loss of ATX to investors, despite what we believe to be its obvious materiality.16 In the petition, ATX alleged that beginning in June 2023, ATX “fail[ed] to make a series of required payments for fiber optic networking products supplied by AAOI” that were “several months past due.” ATX’s response to the Petition claims that AAOI’s invoices contain multiple inaccuracies, including an unexplained starting balance of

$1.7 million, $1.2 million in products that ATX hadn’t been shipped, and $9.1 million in future tariff liabilities.17

“If you want to call it channel stuffing, we used that exact same terminology… I don’t know how that translates into products shipped into the market. We are very suspicious of that.”

According to familiar sources, the suit effectively boiled down to AAOI’s treatment of tariffs, resulting from its practice of shipping products from China through Taiwan for “final assembly” before being shipped to the U.S.

“The concern was really around the strategy that was employed to mitigate tariffs… If you’ve built the product exclusively out of China, you’d pay full tariff. But in some cases, vendors have sourced a portion of the product out of China and maybe done assembly and test, let’s say in Taiwan or in a jurisdiction that was looked upon more favorably from the US at least until probably January in ‘25. That’s probably going to change pretty significantly.”

A second source corroborated these claims:

“…the U.S. Customs essentially said, even though you’re putting this stuff together in Taiwan, it doesn’t meet the requirements for a Taiwanese product. that was how the move to Taiwan and doing more work

in Taiwan came about, was to avoid those tariffs. I think, in general, that this tariff situation over the

next year is going to become very difficult ”

AAOI no longer disclosed ATX as a 10% customer as of Q4 2023, and our conversations suggest ATX is no longer a customer, but now a competitor.

Our Analysis of Import/Export Records Bolsters Concerns of AAOI’s Tariff Practices

Our own review of import/export data from AAOI’s subsidiaries in both China and Taiwan bolsters our concerns regarding the Company’s tariff practices. First, AAOI has historically claimed that most of the Company’s CATV products are produced in China. Consider from CFO Murry on the Company’s Q4 2022 conference call:

AAOI’s disclosures also imply that Digicomm had not paid for the product by year-end, bolstering these concerns. In Q4 2023, AAOI reported total revenues of $60.5 million, missing analyst estimates by $4.7 million. However, had the Company not signed Digicomm, we estimate revenues would have missed by $21.6 million – a massive

difference that would have not only diminished management’s already dismal credibility and fundraising efforts.

- AAOI discloses 10% customers on each quarterly conference call. Historically, AAOI called out a single large CATV customer, which was widely understood to be ATX, as confirmed by the Company’s disclosures in annual reports. However, we believe that in Q4 2023, Digicomm replaced ATX as this customer. AAOI disclosed the customer contributed 28% of total revenues, or $16.9 million, in the quarter, as shown below.19

- AAOI’s 2023 Form 10-K then disclosed that, “As of December 31, 2023, Digicomm represented 2% of total accounts receivable”, implying receivables of $16.9 million of the $48.1 million total – the entirety of Digicomm’s implied Q4 revenues.

DISCLAIMER

By downloading from or viewing material on this website you agree to the following Terms of Service. Use of Culper Research’s (“Culper”) research is at your own risk. In no event should Culper or any affiliated party be liable for any direct or indirect trading losses caused by any information on this site. You further agree to do your own research and due diligence, consult your own financial, legal, and tax advisors before making any investment decision with respect to transacting in any securities covered herein. You should assume that Culper (possibly along with or through our members, partners, affiliates, employees, and/or consultants) along with our clients and/or investors has a position in any securities covered herein. You should assume that following publication of any research, we are likely to immediately transact in these securities (by increasing and/or decreasing positions and/or risk exposure), continue to trade in these securities for an undefined time period thereafter, and be long, short, or neutral at any time hereafter regardless of our initial recommendation, conclusions, or opinions. We trade securities in conjunction with risk tolerances and management practices, and such trading may result in the derisking of some or all of the positions in the securities covered herein, at any time following publication of any report, depending on security-specific, market, portfolio, or other relevant conditions. Culper does not undertake to update or supplement this report to reflect changes in its position. Research may contain estimated fair values of securities, utilizing various valuation methods. Estimated fair values are not price targets, and Culper does not commit to hold securities until such time as the estimated fair values are reached. Culper may change its estimates of fair values at any time hereafter without updating its research or otherwise disclosing updated fair values publicly. We may transact in the covered securities for various reasons, none of which may relate to Culper’s estimates of fair value. Research is not investment advice nor a recommendation or solicitation to buy securities. To the best of our ability and belief, all information contained herein is accurate and reliable, and has been obtained from public sources we believe to be accurate and reliable, and who are not insiders or connected persons of the securities covered herein or who may otherwise owe any fiduciary duty or duty of confidentiality to the issuer. However, such information is presented “as is,” without warranty of any kind – whether express or implied. Culper makes no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results to be obtained from its use. Research may contain forward-looking statements, estimates, projections, and opinions with respect to among other things, certain accounting, legal, and regulatory issues the issuer faces and the potential impact of those issues on its future business, financial condition and results of operations, as well as more generally, the issuer’s anticipated operating performance, access to capital markets, market conditions, assets and liabilities. Such statements, estimates, projections and opinions may prove to be substantially inaccurate and are inherently subject to significant risks and uncertainties beyond Culper’s control. All expressions of opinion are subject to change without notice, and Culper does not undertake to update or supplement this report or any of the information contained herein. You agree that the information on this website is copyrighted, and you therefore agree not to distribute this information (whether the downloaded file, copies / images / reproductions, or the link to these files) in any manner other than by providing the following link — https://culperresearch.com The failure of Culper to exercise or enforce any right or provision of these Terms of Service shall not constitute a waiver of this right or provision. If any provision of these Terms of Service is found by a court of competent jurisdiction to be invalid, the parties nevertheless agree that the court should endeavor to give effect to the parties’ intentions as reflected in the provision and rule that the other provisions of these Terms of Service remain in full force and effect, in particular as to this governing law and jurisdiction provision. You agree that regardless of any statute or law to the contrary, any claim or cause of action arising out of or related to use of this website or the material herein must be filed within one (1) year after such claim or cause of action arose or be forever barred.

REFERENCES

1 Sell-side note #1: “The 4Q24 revenue outlook of ~$99mn is predicated on further 400G increases, particularly from newly returned customer Amazon.” We are increasing 2025 numbers but not yet modeling the

2 As described further on page 6, we believe Amazon moved forward with Jabil, instead. In late September 2024, Amazon announced a “strategic alliance” with Jabil, and in January 2025, Amazon invested directly into Jabil.

3 Sell-side notes echo this view, claiming for example that, “It makes sense that the value proposition AAOI offers to Microsoft would be attractive to others like Alphabet, Meta, Amazon, and Nvidia.”

4 Tellingly, competitors such as Innolight, Fabrinet, and Eoptolink have moved manufacturing to Thailand, a low-cost locale without the tariff risks of China and Taiwan.

5 See comments by CEO Lin on November 2023 and May 2024 conference call: “I think we should get some volume order by late Q3, [indiscernible] order next year, Q1 to Q4 next year. I would say just 800G only is more than $500 million or even $600 million...”

6 See pages 10 to 12 for a summary of our views of AAOI and the previous 100G upgrade cycle.

7 Relevant Quotes. AAOI competitor #1: “It’s about a 6-month cycle.” Competitor #2: “anywhere between 6 months to a year.” Competitor #3: “will take 6 to 9 months.” Competitor #4: “...once you’re qualified, which will take 6 to 9 months...” Hyperscaler #1: “From 1 to 3 months... or for a new vendor, it can take 3 to 6 months.” Hyperscaler #2: “If 400G, qualification should be 3 to 4 months. If 800G or 1.6T, qualification could take 8 to 9 months.”

8 2023 Form 10-K, page 27.

9 See COF Murry’s comments on Q3 2023 conference call, November 2023.

10 CFO Murry, Q3 2024 conference call, November 2024: “...we do expect to continue to invest primarily in the U.S. and Taiwan for manufacturing capacity over the next few quarters, as we noted in our prepared remarks. And that will allow us to continue to execute on the revenue growth trajectory that we outlined.”

11 Capex figures per each company’s annual reports, fiscal year end.

12 For example, per CFO Murry at the March 2018 OFC conference: “Looking ahead to what we see in terms of capital expenditures. So if you look at over the last couple of years, we've had a gradual increase, I think, in CapEx associated with machinery and equipment, especially... It takes time to invest, develop that technology, and then commission and bring up the machinery that does that manufacturing... investments that we're making in our China factory... for manufacturing of transceivers and other optical devices... So we expect that, that facility will be online in the 2020 time frame...”

13 That analyst’s August 2024 note suggested that AAOI could develop “800G capacity to support $600mn to $1+bn in total revenues in 2025 and beyond” with just “$40mn to $60mn” in capital. In the same analyst’s more recent October 2024 note, however, they backtracked from $600-1,000M to just “multiple hundreds of millions of dollars.”

14 CEO Lin stated on the Company’s Q3 2023 call in November 2023 that 800G units are accompanied by “very good ASP, more than $600 or $700, so you can see opportunity next year.” However, industry analysts and participants tell us that as of January 2025, pricing has already fallen to “about $400” and that LPOs are even cheaper at roughly $300. LightCounting contemplates 800G ASPs of $411 in 2025, $334 in 2026, and $318 in 2027.

15 Sell-side notes echo this view, claiming for example that, “It makes sense that the value proposition AAOI offers to Microsoft would be attractive to others like Alphabet, Meta, Amazon, and Nvidia.”

16 23-DCV-308333 FORT BEND COUNTY, TEXAS District Court

17 According to the docket, the parties disclosed a mediated settlement in November 2024.

18 AAOI’s long-lived assets by region were also similar from period to period, suggesting that AAOI did not shift production to Taiwan.

19 AAOI’s disclosures also seem to imply that ATX’s revenue contribution was negative in Q4 2023, as the earlier disclosures imply ATX contributed $35.2 million through Q3 2023, while subsequent annual disclosures imply just $34.0 million for the full year. We speculate that the $1.2 million difference could be attributable to an undisclosed write-down of previously recognized revenues in connection with ATX’s unpaid bills and the resulting litigation.